Experiments

India’s 2019 corporate tax cut illustrates the limits of supply-side optimism. Despite a significant reduction in rates, private investment did not surge. Firms invest when capacity utilisation is high and demand prospects are strong—not merely because taxes are lower. In a weak demand environment, tax savings were largely retained as profits rather than converted into new investment.

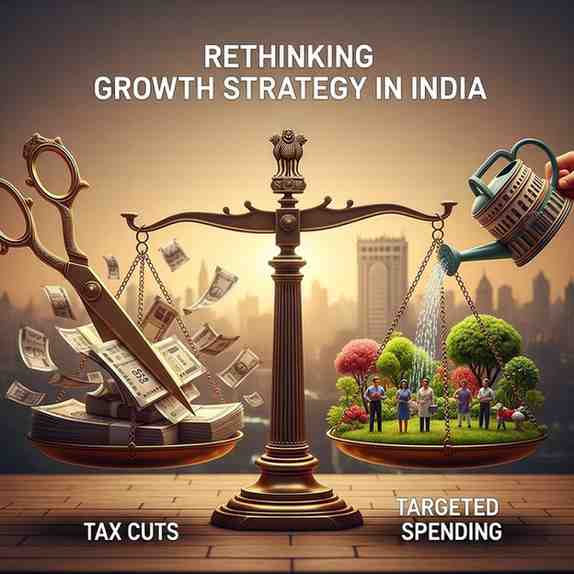

What the Evidence Suggests

From a policy standpoint, a mix of taxation and expenditure tools is sensible. However, the balance of evidence favours expenditure-led strategies. Spending programmes are direct, targeted and aligned with development priorities. Tax cuts rely on behavioural assumptions that vary widely across income groups and economic conditions.

Why Targeting Matters More Than Optics

The choice between tax cuts and spending is not ideological but practical. Expenditure allows governments to identify beneficiaries, anticipate outcomes and link fiscal action to employment, welfare and productivity goals. Tax cuts provide visibility and short-term relief but offer uncertain growth dividends unless supported by job creation and sustained demand.

Conclusion

In an economy where consumption recovery remains fragile, growth is driven less by what the government forgoes in taxes and more by where—and on whom—it spends. India’s development challenge calls for policies that prioritise targeted expenditure, employment generation and public investment over reliance on tax cuts as a standalone growth strategy.

Month: Current Affairs - December 28, 2025

Category: